Call Us Now

Call Us Now Email Us Now

Email Us Now

Across Michigan, many wartime veterans and surviving spouses quietly struggle with the rising cost of aging and long-term care without realizing that a VA pension benefit may already exist to help them.

Families often piece together care however they can. Adult children rearrange work schedules to help parents remain at home. Savings that took decades to build begin disappearing into home care bills, assisted living costs, and medical expenses. Some spouses become full-time caregivers long before they are physically able to manage it. Others pay out of pocket simply because no one ever explained there might be another option available.

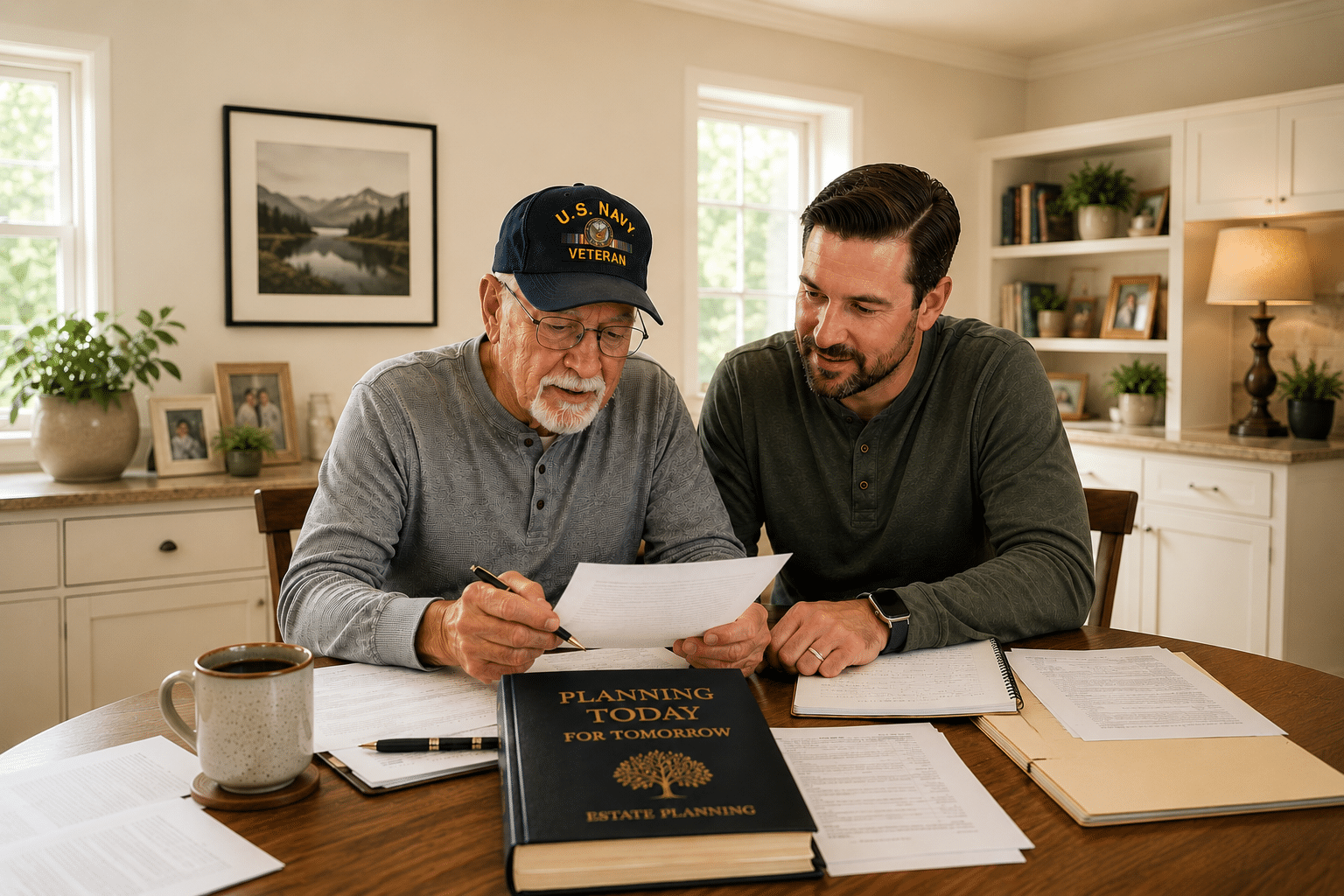

Many veterans never talk much about their military service. For some, it was simply a chapter of life that ended decades ago. They returned home, built careers, raised families, and moved forward. Because of that, many families never connect that long-ago wartime service with benefits that may still be available today.

Unfortunately, families often discover the VA pension benefit only after years of financial strain or after a veteran has already passed away. By then, they are left wondering why they never heard about it sooner.

The benefit exists. The eligibility requirements are real. And many Michigan families may qualify without realizing it.

A BENEFIT THAT WAS ALWAYS THERE

The VA pension benefit, sometimes referred to as Aid and Attendance when additional care assistance is needed, has existed for decades. It is separate from VA disability compensation and is designed specifically to help qualifying wartime veterans and certain surviving spouses offset the cost of long-term care.

Depending on the situation, the benefit may help pay for in-home care, assisted living, memory care, or nursing home services. For families already struggling with those expenses, the monthly benefit can provide meaningful financial relief.

Eligibility depends on several factors, including wartime service, income, assets, and medical or care needs. Veterans who require assistance with daily activities such as dressing, bathing, eating, or mobility may qualify for higher monthly benefit amounts under the Aid and Attendance level.

Surviving spouses may also qualify independently, even if the veteran never applied during their lifetime.

WHO MAY POTENTIALLY QUALIFY

The VA pension benefit is specifically tied to wartime service. Veterans generally must have served during an official wartime period recognized by the Department of Veterans Affairs, including World War II, the Korean War, the Vietnam War, or the Gulf War era. Combat service is not necessarily required.

In addition to service requirements, the VA reviews financial eligibility, including income and assets. There are also medical and functional requirements related to the need for care or assistance with daily living activities.

The rules are detailed and have become more complex in recent years, particularly regarding asset transfers and financial planning. Because of this, many families incorrectly assume they do not qualify without ever fully evaluating their situation.

That assumption can be costly.

WHY SURVIVING SPOUSES ARE OFTEN OVERLOOKED

One of the least understood parts of the VA pension program is that surviving spouses of wartime veterans may still qualify for benefits years after the veteran’s passing.

A widow or widower whose spouse met wartime service requirements may qualify based on their own financial and care needs, even if the veteran never previously received VA benefits.

For many surviving spouses, especially older adults now facing rising care costs alone, the connection between military service decades ago and financial assistance today is not always obvious. In many cases, families only learn about the benefit through community referrals, elder law planning discussions, or after speaking with someone familiar with VA pension eligibility.

WHAT THESE BENEFITS CAN COVER

VA pension benefits are not intended to pay every care expense in full, but they can significantly reduce the financial burden families face.

Depending on the individual situation, the benefit may help offset the cost of in-home caregiving, assisted living communities, memory care services, skilled nursing care, and other forms of support related to daily living needs. For many families, these monthly payments provide meaningful relief at a time when care expenses are steadily increasing.

The pension is generally paid monthly directly to the beneficiary and is not taxable. Unlike reimbursement-based programs, recipients are not typically required to submit receipts for every individual expense.

Still, applying is rarely simple. Families often need service records, medical documentation, financial statements, and detailed supporting information. Errors or incomplete applications can delay approval.

WHY CAREFUL PLANNING MATTERS

VA pension rules have changed substantially over time. In 2018, the VA implemented a three-year look-back period for certain asset transfers, similar in concept to Medicaid planning rules. Financial decisions involving trusts, gifts, annuities, or transferred assets can directly affect eligibility.

That is why families should avoid making assumptions or financial changes without guidance from professionals familiar with both VA pension planning and elder law.

For Michigan families already considering Medicaid planning or long-term care planning, understanding how VA benefits interact with those strategies is especially important.

The families most likely to benefit from VA pension planning are often not the ones who assume they qualify immediately. They are the ones who take the time to ask questions before care costs overwhelm their options.

If your family includes a wartime veteran or surviving spouse facing rising care expenses, it may be worth exploring whether VA pension benefits could help.

Military service may have happened decades ago, but the benefits connected to that service may still matter today.

If your family includes a wartime veteran or surviving spouse managing long-term care costs, Estate Planning & Elder Law Services, P.C. can help evaluate whether VA pension benefits may play a role in your planning strategy.